Major listed companies in artificial intelligence industry:At present, the listed companies in the domestic artificial intelligence industry mainly include BAIDU, TCTZF, BABA and (002230).

Core data of this article:Classification of artificial intelligence, industrial chain of artificial intelligence industry, panoramic atlas of artificial intelligence industry, development course of artificial intelligence industry in China, changes in key directions of artificial intelligence industry, distribution of core technologies of industrial intelligence enterprises, scale of artificial intelligence market in China, application share of artificial intelligence market in China, application of artificial intelligence in various industries, investment and financing of artificial intelligence industry in China, distribution of investment and financing rounds of artificial intelligence industry in China, Supply and demand of talents in various technical directions of artificial intelligence, list of new professional universities of artificial intelligence, urban competitiveness of artificial industry in China, representative enterprise areas of industrial intelligence industry, regional distribution of investment and financing events in artificial intelligence industry in China, competitive factions of artificial intelligence industry in China, development trend of artificial intelligence, scale prediction of artificial intelligence industry in China, number of new generation artificial intelligence innovation and development zones in China.

1. Overview of artificial intelligence industry

— — Definition and classification of artificial intelligence

As a cutting-edge interdisciplinary subject, artificial intelligence is a new technical science that studies and develops theories, methods, technologies and application systems for simulating, extending and expanding human intelligence. It is regarded as a branch of computer science, and its research includes language recognition, image recognition, natural language processing and expert system.

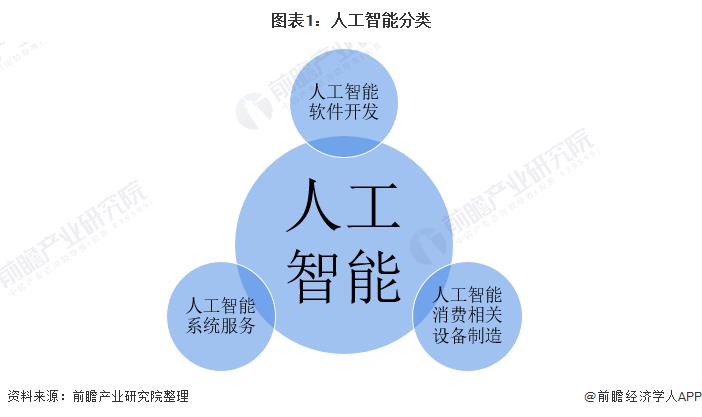

The artificial intelligence industry belongs to a strategic emerging industry. According to the Catalogue of Key Products and Services of Strategic Emerging Industries (2016) issued by the National Development and Reform Commission, China’s artificial intelligence can be divided into three subordinate industries, namely, artificial intelligence software development, artificial intelligence consumption-related equipment manufacturing and artificial intelligence system services.

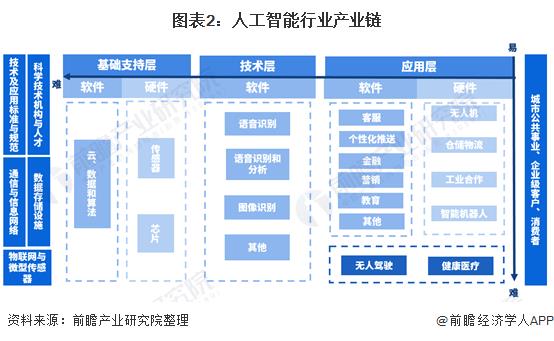

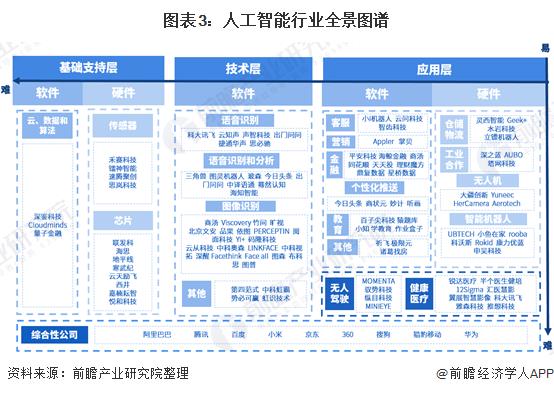

2) Analysis of the industrial chain of artificial intelligence industry: The industrial chain covers a huge industry.

The industrial chain of artificial intelligence includes three layers: basic layer, technical layer and application layer. Among them, the basic layer is the foundation of the artificial intelligence industry, mainly including hardware facilities such as AI chips and infrastructure and data resources of service platforms such as cloud computing, providing data services and computing support for artificial intelligence; The technology layer is the core of the artificial intelligence industry, and the technology path is constructed based on simulating the relevant characteristics of human intelligence. Application layer is an extension of artificial intelligence industry, which integrates one or more basic application technologies of artificial intelligence and forms software and hardware products or solutions for specific application scenarios.

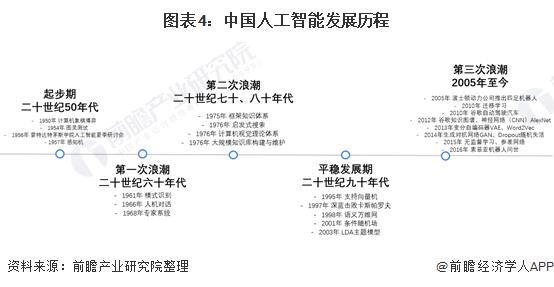

2. The development course of artificial intelligence industry in China: the industry is in the stage of rapid development.

The concept of artificial intelligence was put forward at Dartmouth Conference in 1956. Artificial intelligence has a history of more than 60 years, and has experienced three waves of development since its birth. They are 1956-1970, 1980-1990 and 2000 to the present.

In 1959, Arthur Samuel proposed machine learning, which pushed artificial intelligence into the first development climax. Since then, expert system has appeared in the late 1970s, which indicates that artificial intelligence has moved from theoretical research to practical application.

From 1980s to 1990s, artificial intelligence entered the second development climax with the support of American and Japanese projects. During this period, a series of major breakthroughs were made in mathematical models related to artificial intelligence, such as the famous multi-layer neural network and BP back propagation algorithm, and the accuracy of the algorithm model and expert system were further improved. During this period, the researchers specially designed LISP language and LISP computer, which eventually failed due to high cost and difficult maintenance. In 1997, IBM Deep Blue defeated Garry Kasparov, the world champion of chess, which was a landmark event.

At present, artificial intelligence is in the third development climax, benefiting from the common progress in algorithm, data and computing power. In 2006, Professor Hinton of Canada put forward the concept of deep learning, which greatly developed the artificial neural network algorithm and improved the ability of machine self-learning. Then, the breakthrough of algorithm research represented by deep learning and reinforcement learning, and the continuous optimization of algorithm model greatly improved the accuracy of artificial intelligence applications, such as speech recognition and image recognition. With the popularity of Internet and mobile internet, the global network data volume has increased dramatically, which provides a good soil for the great development of artificial intelligence. The rapid development of information technology such as big data and cloud computing, and the application of various artificial intelligence special computing chips such as GPU, NPU and FPGA have greatly improved the computing ability of machines to handle massive videos and images. With the improvement of algorithm, computing power and data ability, artificial intelligence technology has developed rapidly.

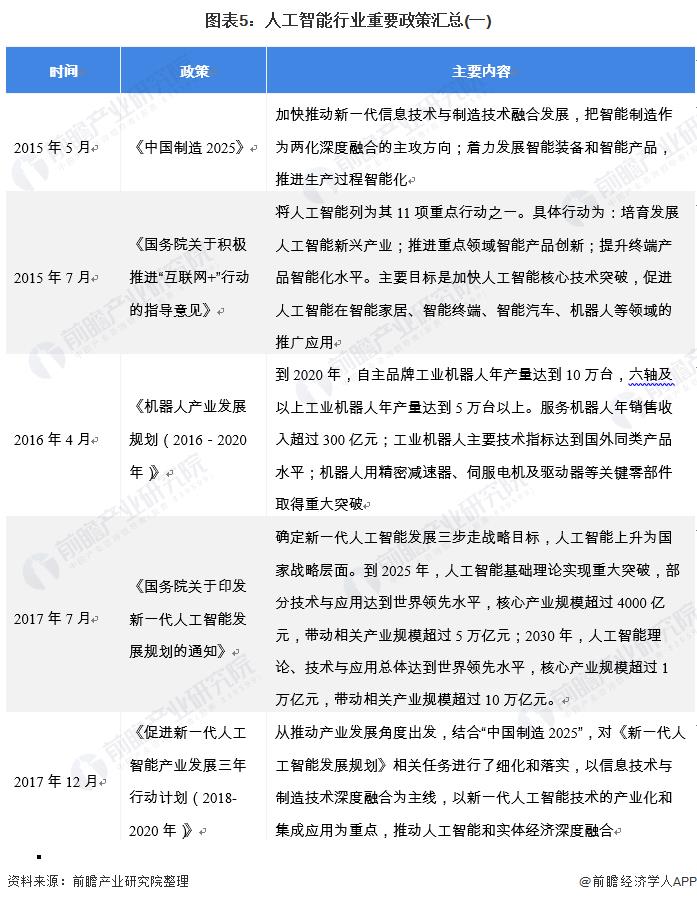

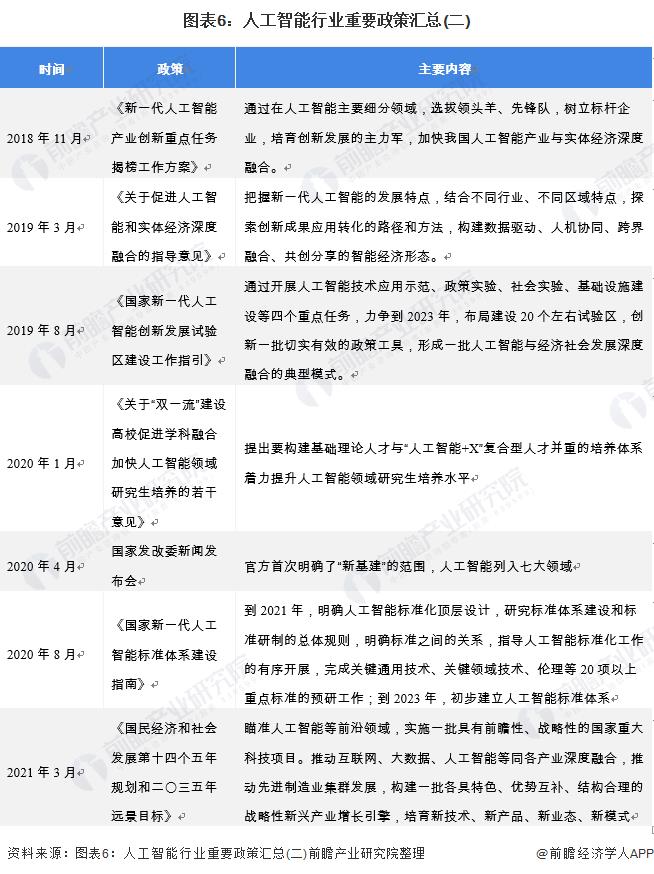

3. Policy background of artificial intelligence industry in China: the industry development has changed from technology to industrial integration.

Before 2017, policies related to artificial intelligence mainly focused on breakthroughs in research and development of artificial intelligence technology. Since 2017, the focus of the policy has shifted from artificial intelligence technology to deep integration of technology and industry. In particular, the "New Generation Artificial Intelligence Development Plan" issued by the State Council in July 2017 clearly pointed out that it is necessary to "accelerate the deep application of artificial intelligence".

From the incomplete summary of the speeches of the two sessions in 2018, it can be seen that the integration of artificial intelligence and industry will be the focus in the future, including official departments such as the Ministry of Science and Technology, the Ministry of Industry and Information Technology, and the Ministry of Civil Affairs, as well as folk representatives such as Baidu, Tencent, and Lenovo, all of which have proposed artificial intelligence+industry, artificial intelligence+medical care, etc.

In 2019, the two sessions even wrote "smart+"into the government work report, and artificial intelligence technology was given the highest level of expectation for the empowerment of society. In the critical period when the industrial economy is changing from quantity and scale expansion to quality and efficiency improvement, the concept of "intelligence+"provides the broadest landing space and return imagination for digital technologies such as artificial intelligence. Opening up the whole chain elements of traditional industrial production through intelligent means can better promote the digitalization, networking and intelligent transformation of manufacturing industry, and can also reverse the iteration and progress of technology itself.

In 2020, it will be clear that artificial intelligence is an important part of the construction of "new infrastructure", and the "Fourteenth Five-Year Plan" points out that it is necessary to promote the deep integration of the Internet, big data and artificial intelligence. And provinces and cities are also vigorously promoting the integration of artificial intelligence and industry, creating application scenarios and demonstration projects.

4. Analysis of the development status of artificial intelligence industry in China.

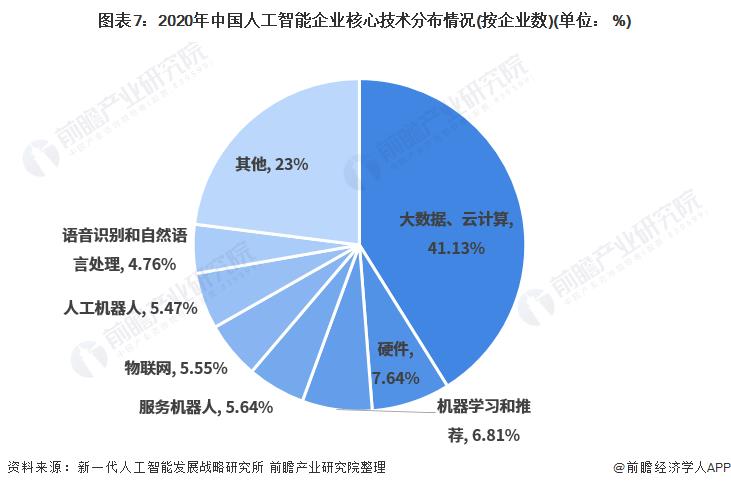

— — Big data and cloud computing are the core technologies with the highest proportion.

From the distribution of core technologies of artificial intelligence enterprises, big data and cloud computing accounted for the highest proportion, reaching 41.13%; Followed by hardware, machine learning, recommendation and service, accounting for 7.64%, 6.81% and 5.64% respectively; Internet of Things, industrial robots, speech recognition and natural language processing accounted for 5.55%, 5.47% and 4.76% respectively.

2) China’s artificial intelligence industry shows a rapid growth trend.

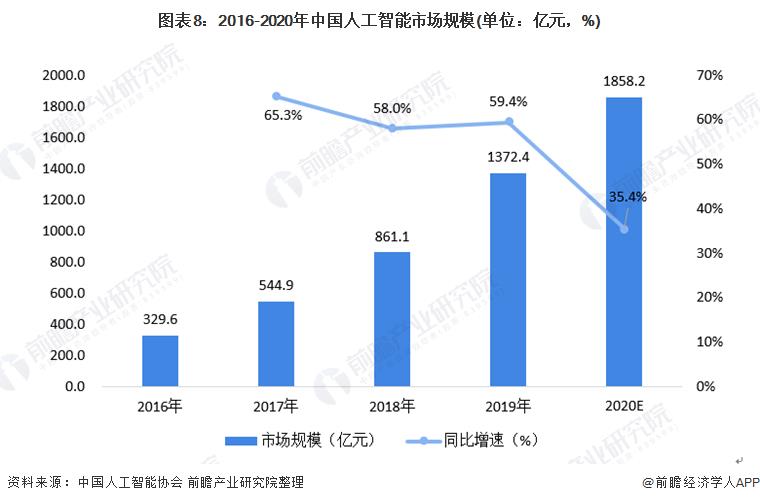

In July, 2017, the State Council issued the "New Generation Artificial Intelligence Development Plan", which raised artificial intelligence to the national strategic level. Thanks to the strong support of national policies and the drive of capital and talents, the development of China’s artificial intelligence industry is at the forefront of the world. It is preliminarily estimated that the market size of artificial intelligence industry in China will be about 185.82 billion yuan in 2020.

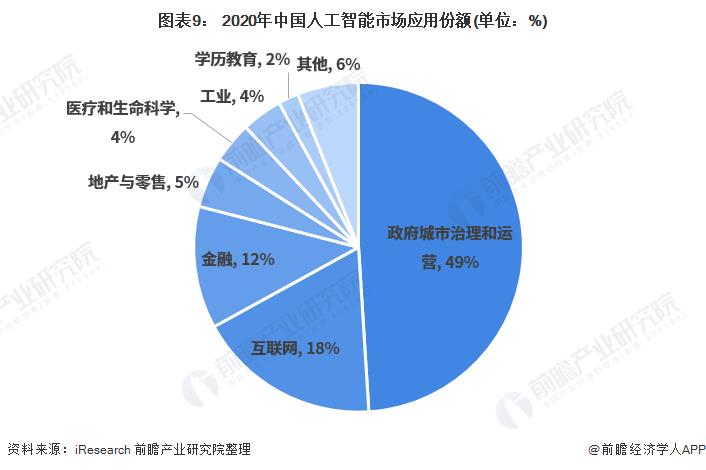

3) The downstream application of artificial intelligence in China mainly focuses on government urban governance and operation.

In 2020, the main customers of China’s artificial intelligence market will come from government urban governance and operation (public security, traffic police, justice, urban operation, government affairs, transportation management, land and resources, prisons, environmental protection, etc.), with applications accounting for 49%, followed by the Internet and financial industries, accounting for 18% and 12% respectively.

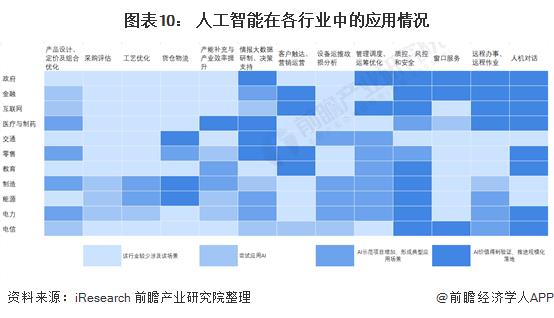

The application of artificial intelligence by enterprises and governments is gradually heating up. Artificial intelligence can be seen in every link that determines the economic benefits of enterprises: AI core helps people live safely, trade remotely and pass easily; Deep learning and knowledge map help enterprises to analyze, predict and make scientific decisions in the production process; Man-machine dialogue improves the user experience in visit registration and service response.

Artificial intelligence will give birth to new technologies, new products, new formats and new models, realize the overall leap of social productivity and push the society into the era of intelligent economy. According to a forward-looking estimate, at present, most large enterprises in China have been planning and investing in artificial intelligence projects continuously, and more than 10% of all enterprises have combined artificial intelligence with their main business to improve their industrial status or optimize their operating efficiency.

4) Capital is more inclined to the early investment of artificial intelligence enterprises

From 2014 to 2020, there were 4,796 investment and financing events in the artificial intelligence industry in China, with a total financing amount of 768.539 billion yuan. In 2014-2018, the financing events and financing scale showed a continuous growth trend. In 2018, the financing amount reached 148.246 billion yuan, and there were 965 financing events.

From 2019 to 2020, the market of China’s artificial intelligence industry is much calmer than before, and the financing events have declined but the financing scale has increased. In 2020, there were 723 investment and financing incidents in China’s artificial intelligence industry with a total amount of 146.837 billion yuan. From January to July, 2021, there were 506 financing events, and the financing amount reached 183.992 billion yuan, which has exceeded the total amount in 2020.

Note: The data of 2021 is as of July 27th.

Judging from the distribution of financing rounds in China’s artificial intelligence industry, because the financing amount and valuation of start-up enterprises are relatively reasonable and the bubble is small, the capital is more inclined to the early investment of artificial intelligence enterprises. From 2014 to 2019, the angel round and A round in the artificial intelligence industry accounted for the highest proportion.

With the gradual maturity of the artificial intelligence market segment, the proportion of early investment gradually decreased, and the investment rounds of artificial intelligence gradually moved back. In 2020, the proportion of Round A will be 42.20%, Round B will rise to 20.22%, and the proportion of Angel Wheel will drop to 9.23%.

Note: The data of 2021 is as of July 27th.

5) There is a shortage of talents in artificial intelligence technology in China, and colleges and universities offer related majors.

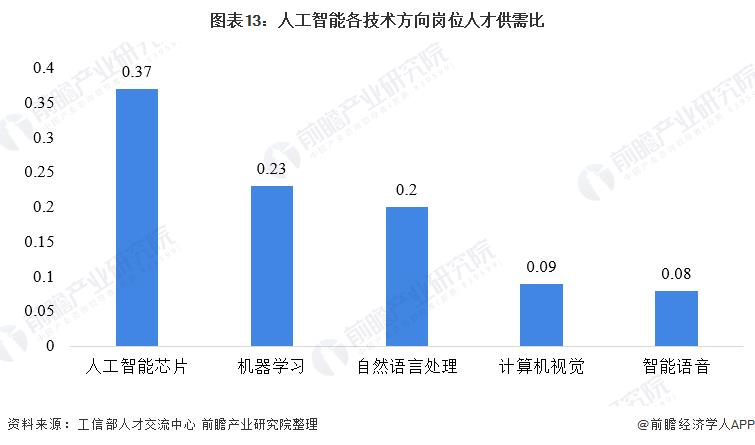

According to the relevant data released by the Ministry of Industry and Information Technology, the ratio of supply and demand of talents in different technical directions of artificial intelligence is lower than 0.4, indicating that the supply of talents in this technical direction is seriously insufficient. From the perspective of sub-industries, the supply-demand ratio of post talents for intelligent voice and computer vision is 0.08 and 0.09 respectively, and relevant talents are extremely scarce.

Note: the ratio of supply and demand of post talents = the number of talents who intend to enter the post/the number of posts.

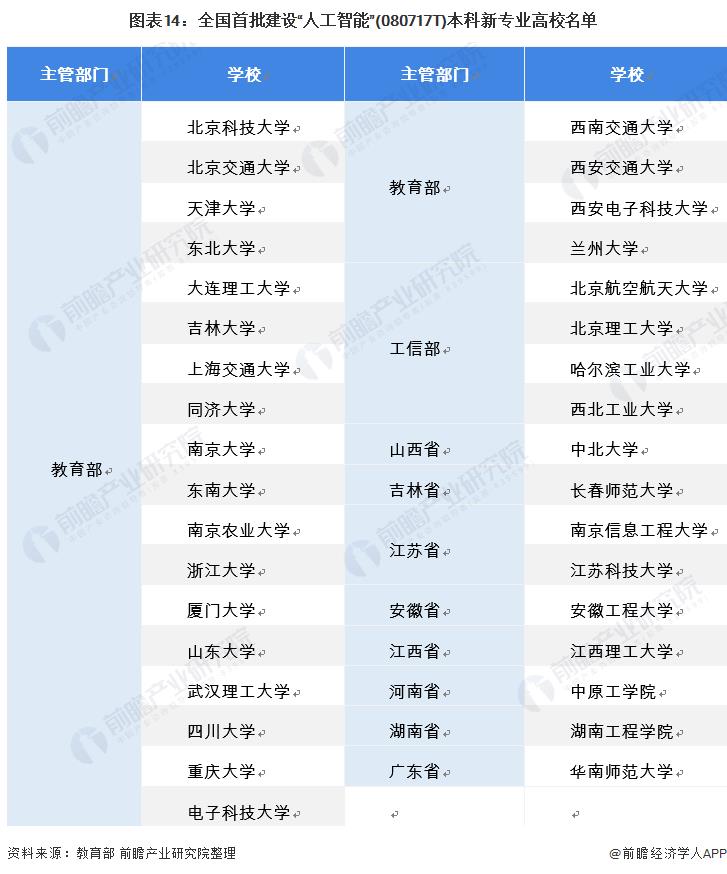

Compared with foreign countries, the cultivation of artificial intelligence in colleges and universities in China started late, but in recent years, the disciplines and majors of artificial intelligence in China have been accelerated, and a multi-level artificial intelligence talent training system has gradually formed. In April 2018, the Action Plan for Artificial Intelligence Innovation in Colleges and Universities issued by the Ministry of Education proposed that 50 artificial intelligence colleges, research institutes or interdisciplinary research centers should be established by 2020.

In 2019, the Ministry of Education issued the "Notice of the Ministry of Education on Announcing the Record and Approval Results of Undergraduate Majors in Ordinary Colleges and Universities in 2018". A total of 35 colleges and universities across the country were awarded the first batch of qualifications for building "artificial intelligence" undergraduate majors.

5. Analysis of the competitive pattern of artificial intelligence industry in China.

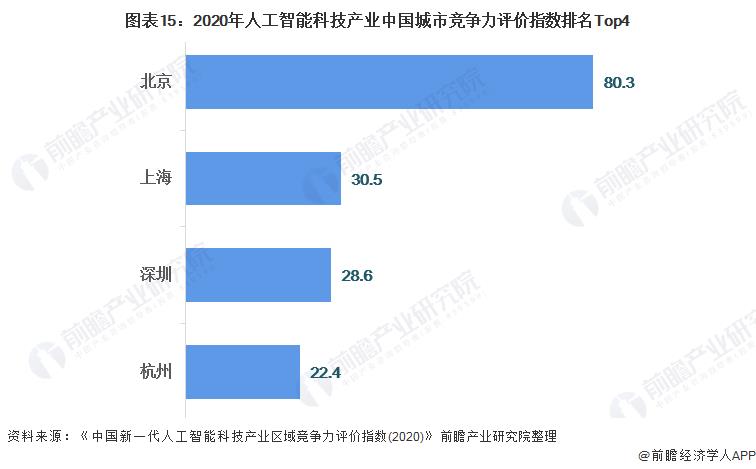

— — Regional competition pattern: Beijing’s artificial intelligence competitiveness is far ahead.

Since 1990, the urban pattern of the development of artificial intelligence industry in China has changed several times. At present, Beijing, Shanghai, Shenzhen, Hangzhou and other cities are performing stably. These cities regard electronic information industry as one of the pillar industries and rank high in the development of Internet industry. These cities all strengthen the advantages of scientific research and talents, accelerate the supplement and improvement of artificial intelligence itself and industry-oriented industrial chain, build demonstration intelligent application scenarios, forward-looking layout of artificial intelligence-related standard systems, promote the sharing of public resources, improve urban environment and livability, and support systematic and advanced R&D layout, which will become the planning direction for cities to grasp the great historical opportunity of artificial intelligence development.

Among them, Beijing is far ahead of other cities in the ranking of competitiveness evaluation index of artificial industry cities in China with 80.3. The second-ranked Shanghai index is 30.5, followed by Shenzhen and Hangzhou with 28.6 and 22.4 respectively.

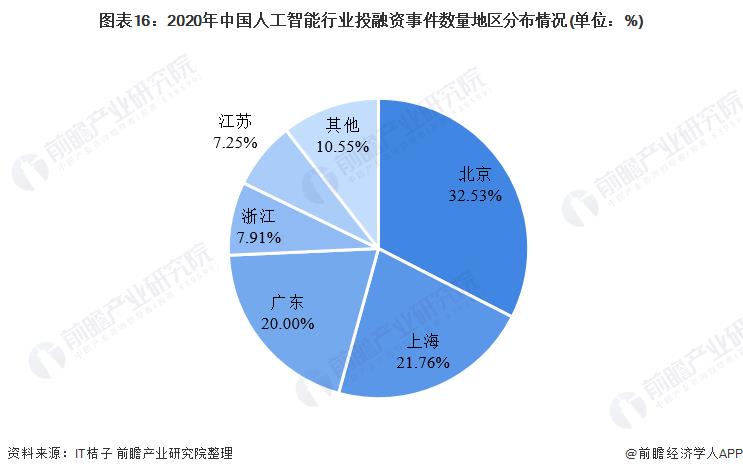

Judging from the territorial distribution of representative enterprises in the artificial intelligence industry, Beijing and Shenzhen are the concentrated places of representative enterprises in artificial intelligence. At the same time, Beijing is also the region with the largest number of investment and financing events in the artificial intelligence industry in 2020. In 2020, Beijing, Shanghai and Guangdong gathered 74.29% of the national AI investment and financing events, of which Beijing accounted for 32.53%, Shanghai for 21.76% and Guangdong for 20%. Zhejiang and Jiangsu followed closely, accounting for 7.91% and 7.25% respectively.

In terms of urban strongholds, four domestic first-tier cities, namely, Beijing, Shenzhen, Shanghai and Hangzhou, have become the focal points for the development of China’s artificial intelligence industry, promoting the rise of artificial intelligence technology in Beijing-Tianjin-Hebei Development Zone, Guangdong-Hong Kong-Macao Greater Bay Area and Yangtze River Delta Economic Zone, and covering the whole country.

2) Enterprise competition pattern: There are many participants, mainly divided into three factions.

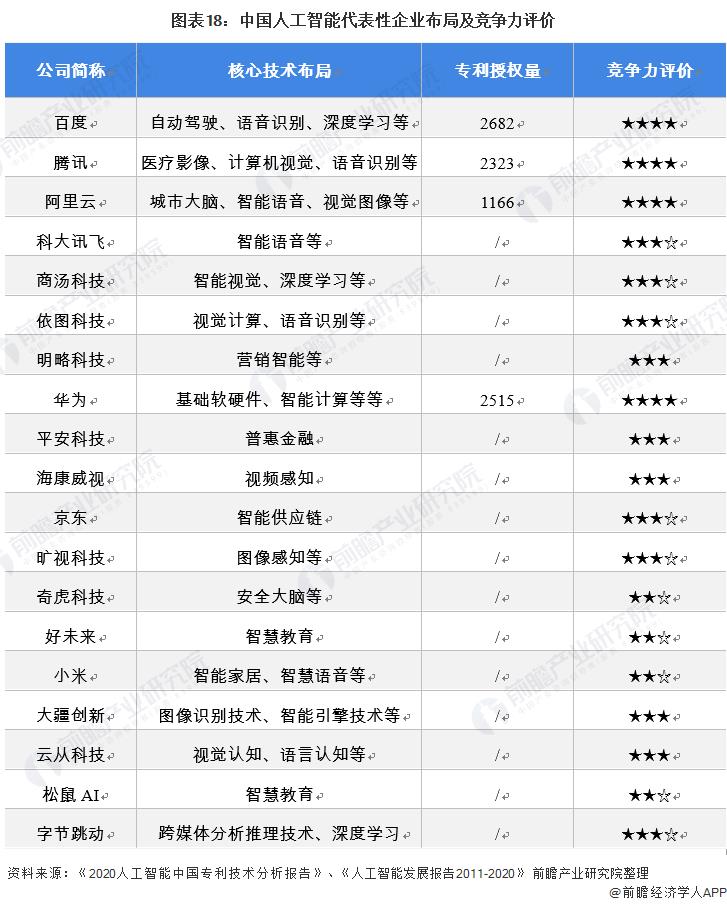

Judging from the competition of enterprises, China’s artificial intelligence enterprises can be mainly divided into three factions, namely, head platform representative enterprises, integrated industry active enterprises and technical level representative enterprises.

The representative enterprises of artificial intelligence platform mainly include Baidu, Alibaba Cloud, Tencent, Huawei, JD.COM and Huawei; Xiaomi, Ping An Technology, Suning and Didi are more active enterprises in the integration industry; Representatives of technical enterprises include Shangtang Technology, Defiance Technology, Yuncong Technology and Yitu Technology as unicorn companies.

Judging from the core technology layout of artificial intelligence enterprises, Baidu, Tencent, Alibaba Cloud, Huawei and other head platform enterprises have laid out a number of AI technologies; However, converged companies such as Ping An Technology, JD.COM, Xiaomi, etc., their technical layout is mainly aimed at the application layer, with strong pertinence.

Judging from the number of patents granted, as of October 2020, Baidu, Huawei and Tencent ranked the top three in the country respectively, indicating that these three companies have strong technology research and development capabilities.

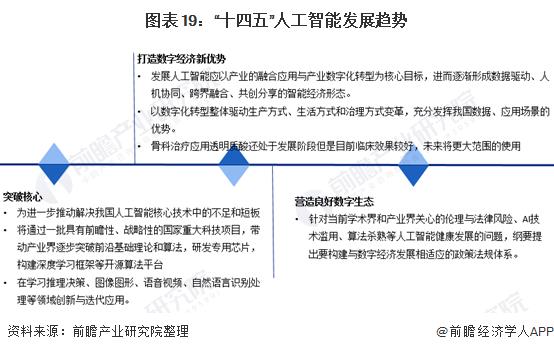

6. Development prospect and trend forecast of artificial intelligence industry in China.

— — The "Tenth Five-Year Plan" construction continued to advance, with high quality, modernization and intelligent development.

In recent years, artificial intelligence has had a significant and far-reaching impact on economic development, social progress and international political and economic structure. The 14th Five-Year Plan for National Economic and Social Development in People’s Republic of China (PRC) and the Outline of Long-term Goals in 2035 have made arrangements for the development goals, core technological breakthroughs, intelligent transformation and application, and safeguard measures of artificial intelligence in China during the 14th Five-Year Plan and the next decade.

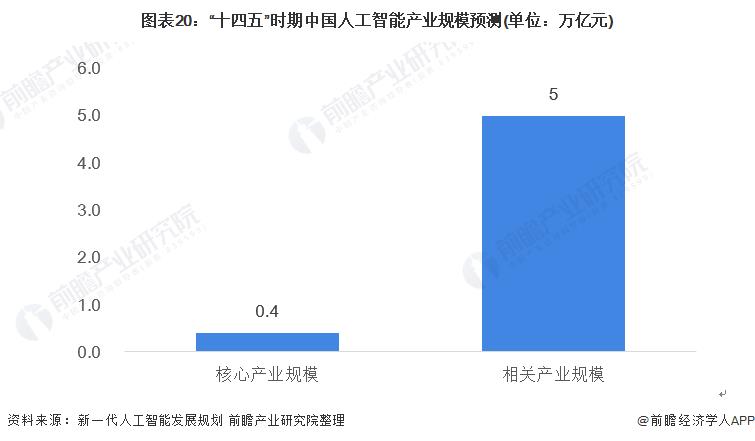

2) The scale of artificial intelligence core industry in China has reached 400 billion, and 20 experimental areas have been laid out.

According to the "New Generation Artificial Intelligence Development Plan", by 2025, China’s basic theory of artificial intelligence has achieved a major breakthrough, and some technologies and applications have reached the world’s leading level. Artificial intelligence has become the main driving force for China’s industrial upgrading and economic transformation, and the construction of intelligent society has made positive progress. The scale of artificial intelligence core industries will exceed 400 billion yuan, driving the scale of related industries to exceed 5 trillion yuan; By 2030, China’s artificial intelligence theory, technology and application will reach the world’s leading level.

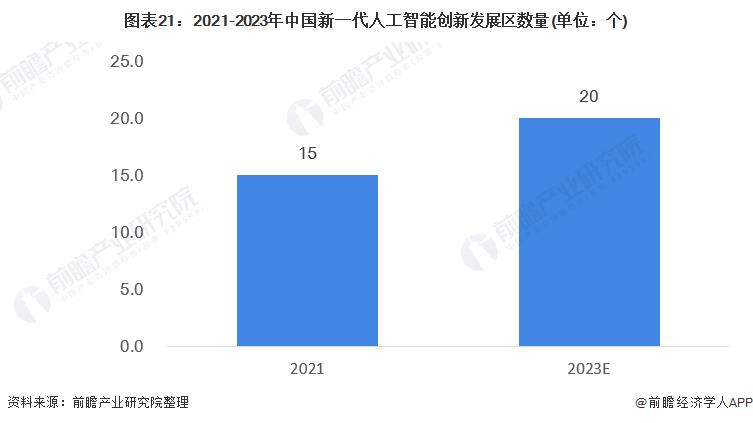

In addition, in order to speed up the implementation of the "Notice of the State Council on Printing and Distributing the Development Plan of the New Generation Artificial Intelligence", the Ministry of Science and Technology issued the "Guidelines for the Construction of the National New Generation Artificial Intelligence Innovation and Development Experimental Zone" in August 2019, aiming at promoting the construction of the National New Generation Artificial Intelligence Innovation and Development Experimental Zone in an orderly manner. By the end of March 2021, 14 cities and 1 county in China had been approved to build the experimental area; By 2023, the number of experimental areas is expected to reach about 20.

Please refer to Foresight Industry Research Institute for the above data and analysis. At the same time, Foresight Industry Research Institute also provides solutions such as industrial big data, industrial research, industrial chain consultation, industrial map, industrial planning, park planning, industrial investment attraction, IPO fundraising feasibility study, IPO business and technology writing, and IPO working paper consultation.

![Car Channel [April 9] [Headlines Red Bar]](http://www.sincy.net.cn/wp-content/uploads/2023/12/PreDnELQ.jpg)

![Car Channel [April 9] [Headlines Red Bar]](http://www.sincy.net.cn/wp-content/uploads/2023/12/vXM581Bm.jpg)

![Car Channel [April 9] [Headlines Red Bar]](http://www.sincy.net.cn/wp-content/uploads/2023/12/muwnSWUg.jpg)

![Car Channel [April 9] [Headlines Red Bar]](http://www.sincy.net.cn/wp-content/uploads/2023/12/NK1AWBVU.jpg)

![Car Channel [April 9] [Headlines Red Bar]](http://www.sincy.net.cn/wp-content/uploads/2023/12/443xB18f.jpg)